Roof Replacement Estimate vs. Final Cost: Why Supplements Close the Gap

Kelvin Spratt

Founder, Supplement Snap · March 10, 2026

Annual Revenue Left Behind

$192,000–$288,000

For a contractor doing 8-12 insurance roofs/month without supplements

Key Takeaways

Why the initial roof replacement estimate is always lower than the final cost, what gets missed in adjuster inspections, and how supplements bridge the gap between estimate and actual cost.

Why the initial estimate is always lower than the final cost

If you've been in the roofing business for any length of time, you already know this: the insurance adjuster's initial estimate almost never covers the full cost of replacing the roof. The estimate comes in at $9,500, but by the time your crew finishes the job, the actual cost is $12,000 or more.

This gap between the initial estimate and the final cost isn't a mistake, and it isn't the adjuster being dishonest. It's a structural reality of how insurance roof inspections work. The adjuster inspects the roof from the surface. They walk it, note visible damage, and write an estimate based on what they can see. They don't tear off the shingles. They don't inspect the decking underneath. They don't check whether the flashing behind the chimney has corroded or whether the ice and water shield in the valleys has deteriorated.

The initial estimate covers the visible scope. The actual job includes everything hidden underneath. That's where the gap comes from, and it's why supplements exist: to close it.

What gets missed in adjuster inspections

Insurance adjusters are not trying to shortchange you. They're writing an estimate based on a surface-level inspection, and there's a long list of items that cannot be assessed without removing the existing roofing materials.

The most commonly missed items include:

Rotted decking: Plywood or OSB that has deteriorated from years of moisture penetration. The shingles on top may look fine, but the wood underneath is soft, spongy, or crumbling. On average, contractors find 2–4 sheets of damaged decking per job, adding $140–$280 to the actual cost.

Failed step and counter flashing: Metal flashing at chimneys, walls, and dormers corrodes over time behind the shingles, invisible from the surface. Replacing flashing at a single chimney can add $200–$500.

Missing or deteriorated ice and water shield: Many older roofs were installed before current building codes required ice and water shield in valleys, at eaves, and around penetrations. This can add $200–$500 depending on coverage area.

Cracked pipe boots: Rubber gaskets around plumbing vents crack and split with age. At $85 per boot with 2–5 boots per roof, this adds $170–$425.

Additional layers of roofing: The original estimate may have been written for a single-layer tear-off. Additional layer removal on a 25-square roof adds $950–$1,375.

Missing drip edge: Older homes often lack drip edge entirely. Full perimeter replacement runs $150–$400.

The real numbers: estimate vs. actual cost

Let's put real numbers to this. Consider a typical 25-square residential roof replacement on a home built in the early 2000s with storm damage.

The adjuster's initial estimate:

Tear-off (1 layer): $1,125

New architectural shingles: $4,500

Felt underlayment: $625

Ridge cap: $375

Pipe boot replacement (1 visible): $85

Haul debris: $562

O&P (20%): $1,454

Total initial estimate: $8,726

What the crew finds during tear-off:

3 sheets of rotted decking along the eave: $209

Corroded step flashing at the chimney (24 LF): $210

Missing ice and water shield in both valleys (180 SF): $333

2 additional cracked pipe boots: $170

Missing drip edge along the rakes (45 LF): $191

O&P on additional items (20%): $223

Total hidden damage: $1,336

The actual cost is now $10,062, a gap of $1,336. On more complex roofs with multiple penetrations, steep pitches, or older construction, this gap can easily reach $2,500–$4,000.

Multiply that across every insurance job you do. If you're running 8–12 insurance roofs per month and the average gap is $2,000, that's $192,000–$288,000 per year in work you're doing but not getting paid for, unless you submit supplements.

How supplements bridge the gap

A supplement is the formal mechanism for closing the gap between the initial estimate and the actual cost. It's a documented request to the insurance carrier saying: your adjuster estimated the visible damage accurately, but our crew found additional concealed damage during tear-off that needs to be covered.

A well-documented supplement includes:

Photographs of each concealed damage finding, taken during tear-off before new materials cover it up

A professional narrative explaining what was found, where it was located, why it was concealed, and why the repair is necessary

Xactimate line items with the correct codes, quantities, and current pricing

Building code references where applicable

When submitted properly, supplements have a high approval rate. Adjusters expect them because they know their surface inspection doesn't catch everything. The key word is 'properly.' A supplement with clear photos, a detailed narrative, and accurate Xactimate formatting gets approved. A supplement with a blurry photo and 'found some bad decking' gets denied.

The difference between contractors who consistently recover supplement revenue and those who don't comes down to documentation quality and submission speed.

Real scenarios: estimate vs. final with supplements

Three scenarios based on common job types:

Scenario 1: Simple ranch home, 20 squares

Initial estimate: $7,200

Hidden damage: 2 sheets rotted decking, 2 cracked pipe boots, missing drip edge on front eave

Supplement value: $680 + O&P = $816

Final cost with supplement: $8,016

Revenue recovered: 11% above initial estimate

Scenario 2: Two-story colonial, 30 squares, chimney and dormers

Initial estimate: $12,800

Hidden damage: 4 sheets rotted decking, corroded step flashing at chimney and 2 dormers, missing ice and water shield in valleys, 3 cracked pipe boots

Supplement value: $2,180 + O&P = $2,616

Final cost with supplement: $15,416

Revenue recovered: 20% above initial estimate

Scenario 3: Complex multi-level, 35 squares, multiple layers

Initial estimate: $14,500

Hidden damage: 6 sheets rotted decking, second layer of shingles, deteriorated ice and water shield, corroded flashing at 2 walls, 4 cracked pipe boots, missing drip edge full perimeter

Supplement value: $4,340 + O&P = $5,208

Final cost with supplement: $19,708

Revenue recovered: 36% above initial estimate

In every scenario, the supplement represents real work the contractor has to do regardless. The only question is whether they get paid for it.

How to systematically capture the difference on every job

Recovering supplement revenue can't happen only when someone in the office remembers. It needs to be a systematic part of your production workflow.

Here's what a systematic supplement process looks like:

Train every crew to recognize and document hidden damage during tear-off: rotted decking, corroded flashing, deteriorated pipe boots

Establish a documentation protocol: when damage is found, stop and photograph it before covering it with new materials. Wide-angle context shot and close-up detail shot.

Use a tool that makes documentation fast and easy. If it takes 20 minutes per finding, your crew won't do it. If it takes 30 seconds to snap a photo and tag the damage type, they'll do it every time.

Generate the supplement report the same day. Don't let findings sit in someone's camera roll for a week.

Track supplement status for every job: submitted, pending, approved, denied. Follow up weekly.

The contractors who build this into their standard workflow recover supplements on 70–90% of their insurance jobs. Those who treat it as an afterthought recover on maybe 10–20%.

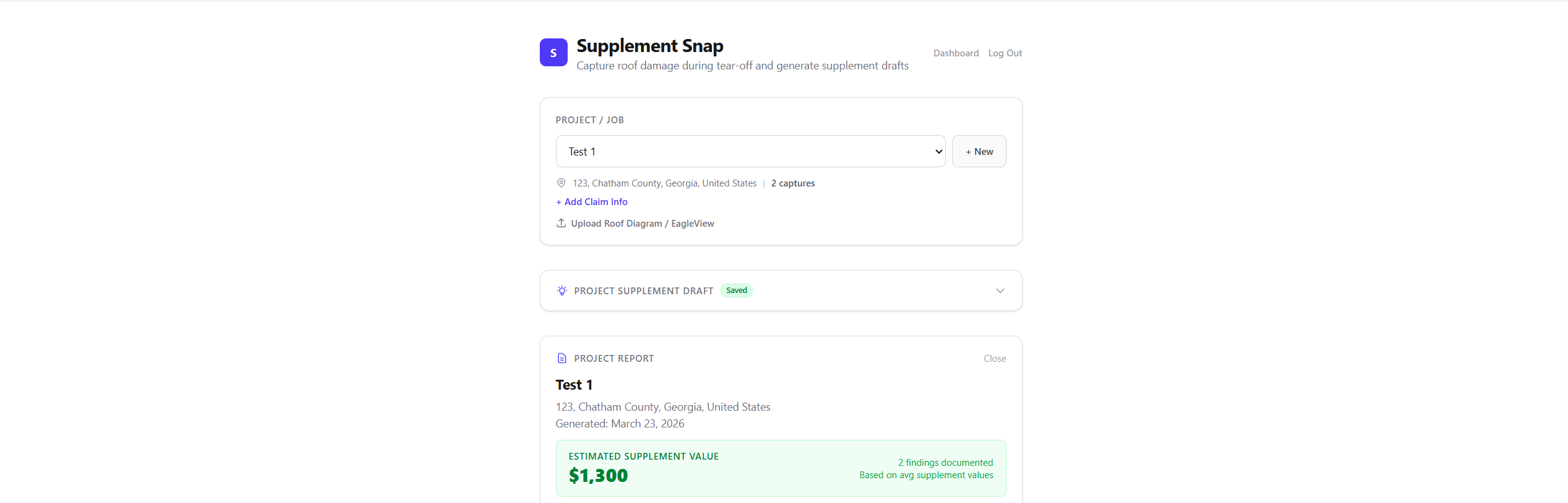

Close the gap with Supplement Snap

Supplement Snap was built to make this systematic approach effortless. During tear-off, the crew opens the app and captures each finding: a photo tagged with the damage type and roof area, plus an optional voice note. Voice notes work in any language. Spanish-speaking crews describe findings in Spanish and the system auto-translates to English.

From that field data, Supplement Snap generates everything you need:

A professional supplement narrative for each finding, written in the language adjusters expect

Xactimate line items with correct codes, quantities, and current regional pricing

An Xactimate-compatible CSV export the adjuster can import directly

A branded PDF report with photos, narratives, findings summary, and line items, ready to email

The entire process from capturing damage on the roof to emailing a complete supplement report takes minutes, not days. Your crew does what they're already doing (finding damage during tear-off) and Supplement Snap turns those findings into revenue.

The gap between the initial estimate and the final cost will always exist. The question is whether you have a system to capture it. With Supplement Snap, every hidden finding becomes a documented, submitted, trackable supplement, and you get paid for the work you're actually doing.

Curious about actual supplement values? See how much roofing supplements pay.

References & Resources

Ready to streamline your supplement process?

Supplement Snap helps your crew capture hidden damage during tear-off and generate adjuster-ready reports in minutes.

Written by

Kelvin Spratt

Founder, Supplement Snap

Kelvin builds software for roofing contractors who are tired of leaving supplement money on the table. His background in software development and insurance restoration workflows drives everything Supplement Snap does.